Rangers Accounts Review – FY20

Despite the current Covid-19 pandemic, Rangers accounts released last week was very much a similar story to previous years under the current regime as we continue our recovery from 2012. I will take a deep dive into this year’s accounts and give some more detail into what they mean for the club.

Revenue

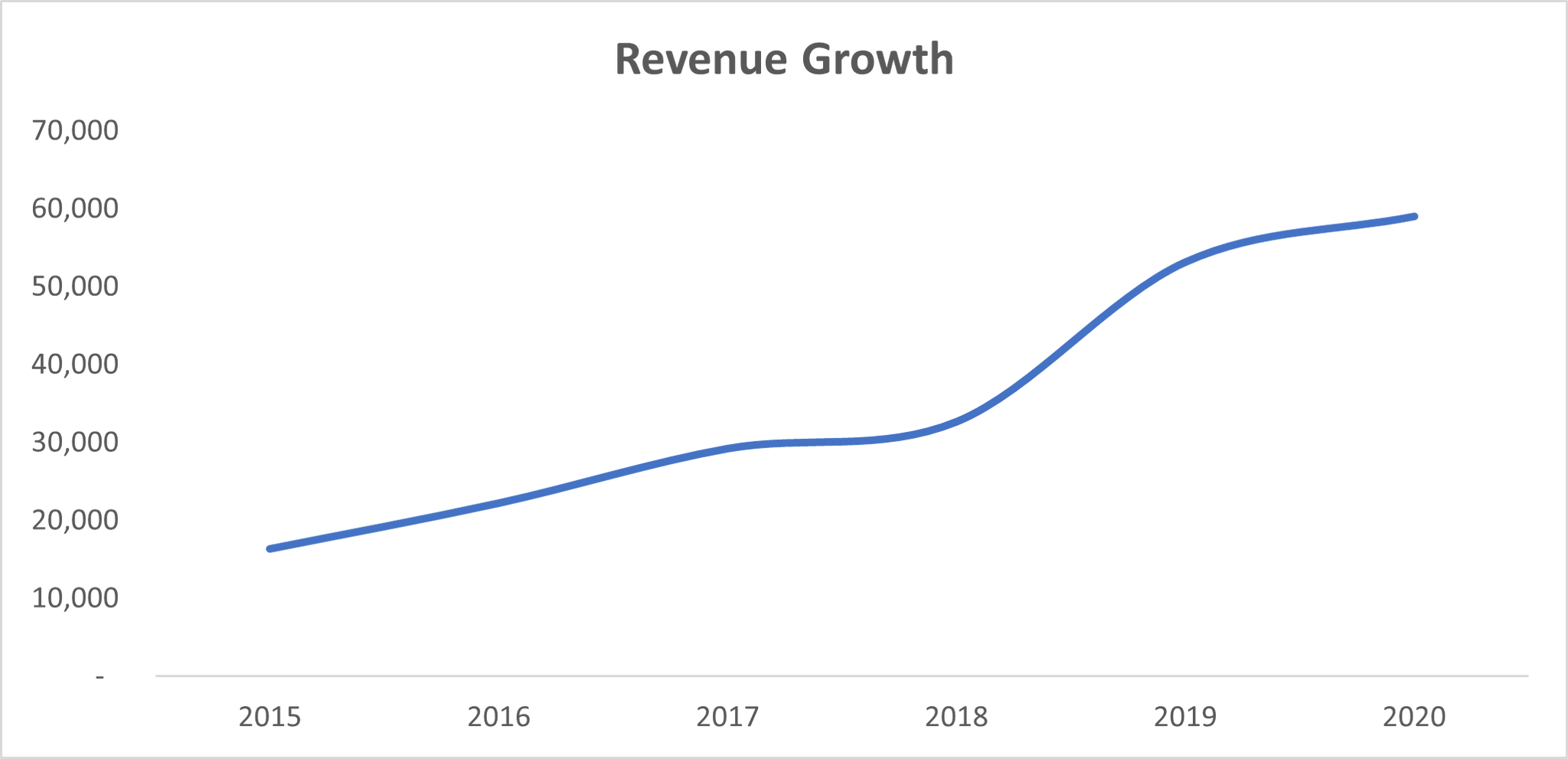

Once again, Rangers demonstrated strong revenue growth from £53.2m in FY19 to £59.0m in FY20, an 11% increase. This is a far cry from the £16.3m in FY15 when the current regime took control of the club. Revenue has increase at an average of 29% per year since FY15.

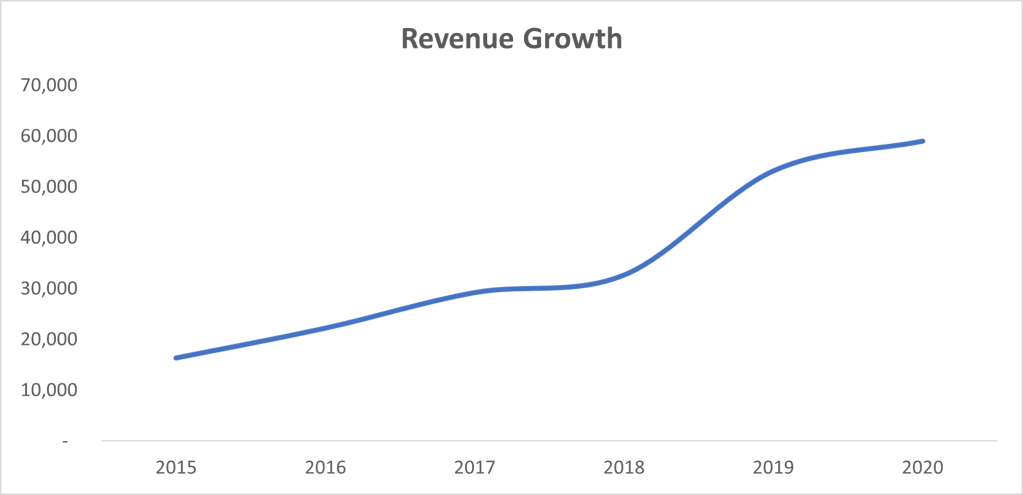

This year’s growth has come from our better performance in the Europa League with two more home games (Braga & Bayer Leverkusen) generating additional ticketing income and UEFA prize money for qualifying. The Europa League campaign was worth £20.7m in FY20 (35% of revenue) versus £14.7m in FY19, highlighting just how critical qualification is to the club. With an ever increasing co-efficient, both club and country, qualification for the Europa League group stage should begin to become the minimum we can expect each year. Other revenue streams such as sponsorship and broadcasting showed modest increases.

The newly launched MyGers scheme is not included nor is any income from Castore – these will both be included in next years accounts.

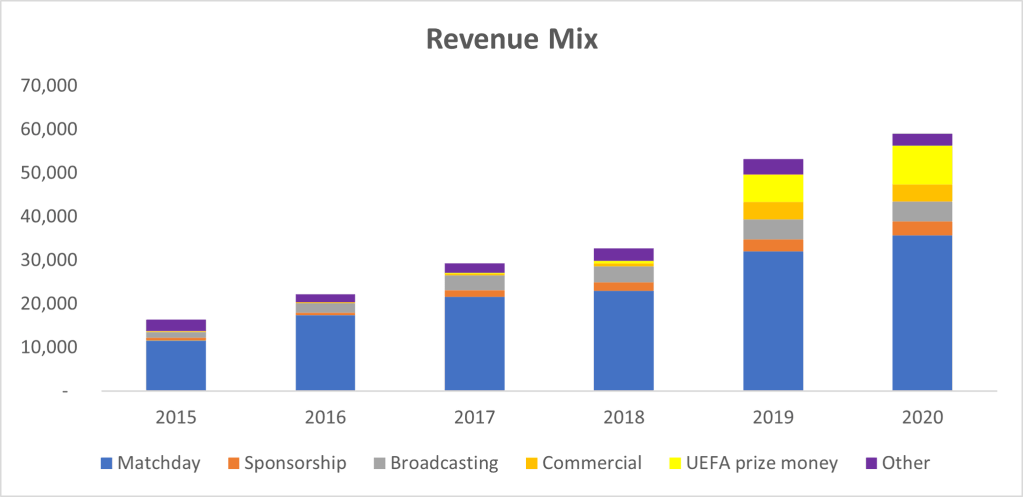

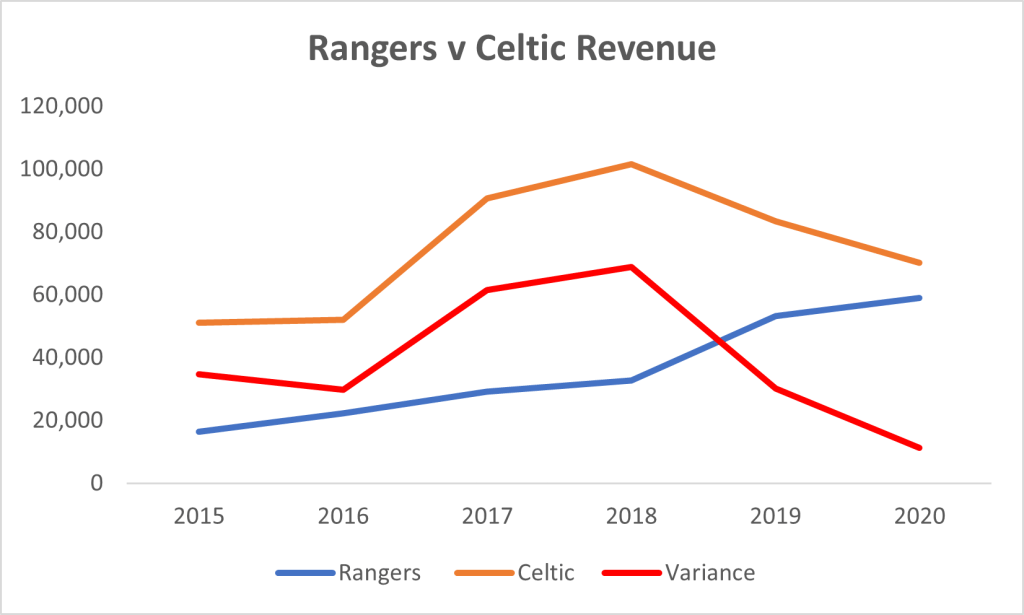

This brought the club as close as we have been since pre-2012 to our closest rivals, with a £11m revenue gap compared to a £69m gap in 2018.

Not included within revenue is £1.25m we have received as part of our Business Interruption Insurance for losses caused by Covid-19. Further claims have been made with timing and scale uncertain.

Expenditure

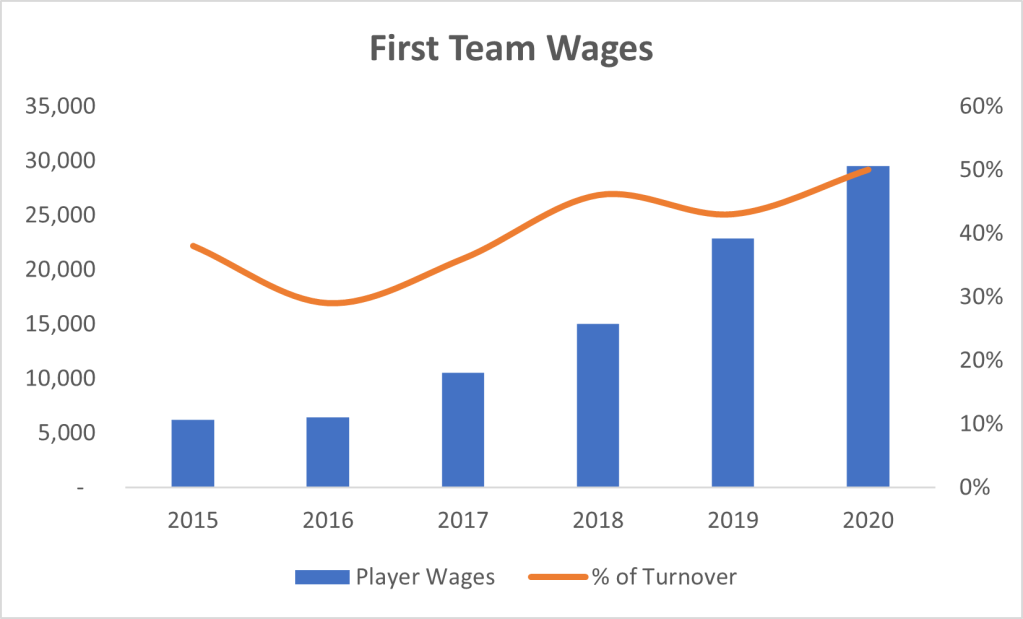

The club’s biggest expenditure is salary costs. We have seen a huge increase in first team wages from £6.2m in FY15 to £29.5m in FY20. Our first team wages to turnover ratio was 50% which is an increase on 43% in the prior year.

Non-first team wages were £13.8m giving a total salary cost for the year if £43.3m (73% of turnover). For reference, of the SPFL Premiership clubs that produce full accounts this would see us with the 4th highest total wage/turnover ratio with Motherwell (87%), St Mirren (80%) and Celtic (77%).

Player Acquisitions and Amortisation

Rangers have invested heavily in the playing squad over the last four years with an average spend each year of £10.2m. FY20 player acquisitions totalled £11.0m. As a result of the continued investment in the playing squad, player amortisation has increased as well. In layman terms, when a football club sign a player, they do not expense the full transfer fee to the profit or loss account. Instead, it is included on the balance sheet and released over the length of the player’s contract. As an example, the £8m transfer fee for Ryan Kent will be expensed at £2m per year of the four years of his contract.

Operating Loss

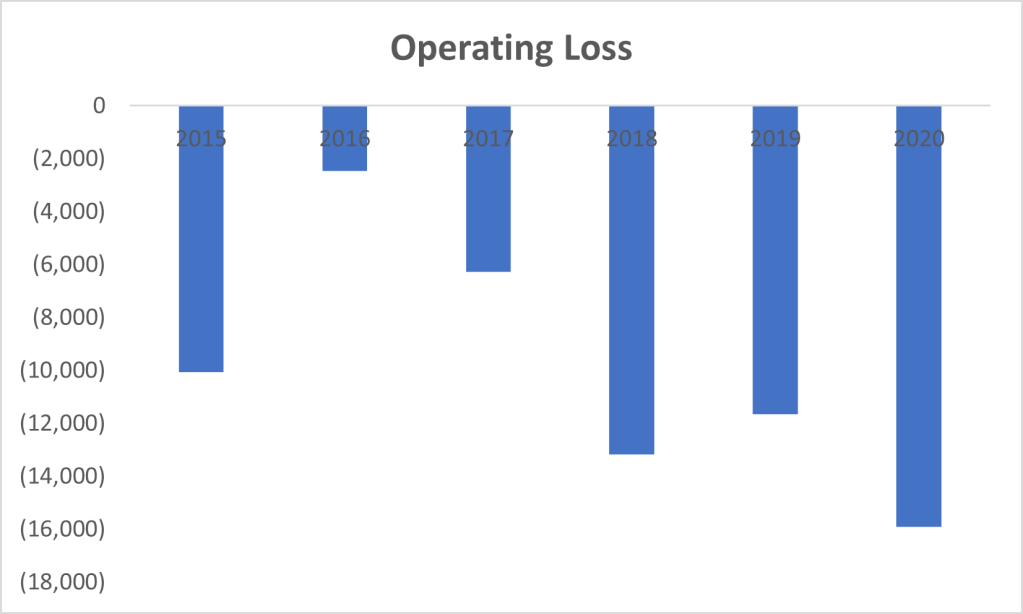

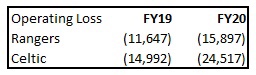

The headline figure of an operating loss of £15.9m follows on from similar losses in FY18 and 19 of £13.2m and £11.6m, respectively. Despite the increase in revenue, the increased operating loss is driven by the abovementioned increased salary costs and player amortisation.

Interestingly, our operating loss in FY19 & 20 was lower than Celtics. However, they have been extremely good at player trading, a core part of their business model, selling Moussa Dembele and Kieran Tierney as well as the compensation received from Leicester when Brendan Rodgers left. To put it bluntly, since FY15, Celtic have sold £80m worth of players – their strategy has been a resounding success from a financial perspective. It is probably the final piece of the jigsaw that we need to get right on our recovery – more on this later.

Infrastructure

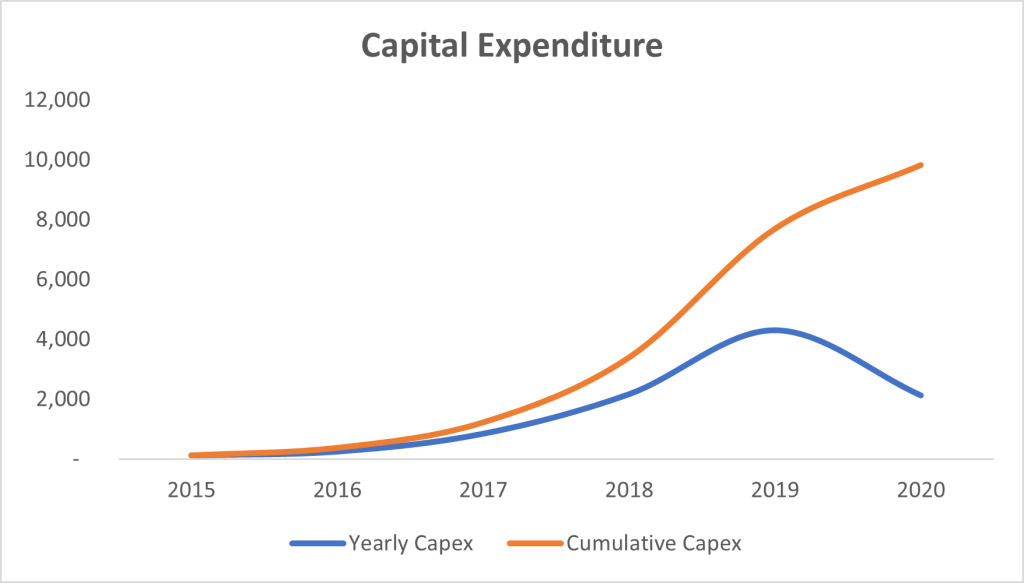

A further area of significant investment within the club has been within infrastructure namely improvements to the stadium and training centre. A further £2.1m was spent in FY20 taking the cumulative spend since FY15 to £9.8m. This will only increase, with current capital commitments of £6.9m mostly relating to the construction of a new facility replacing Edmiston House that is now under construction. This was due to be funded by the partial sale of the Albion car park however that has not happened, yet. Anybody who has been at Ibrox will have undoubtedly noticed the huge amounts of work going on to repair the stadium after years of underinvestment.

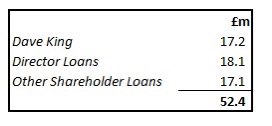

Investors

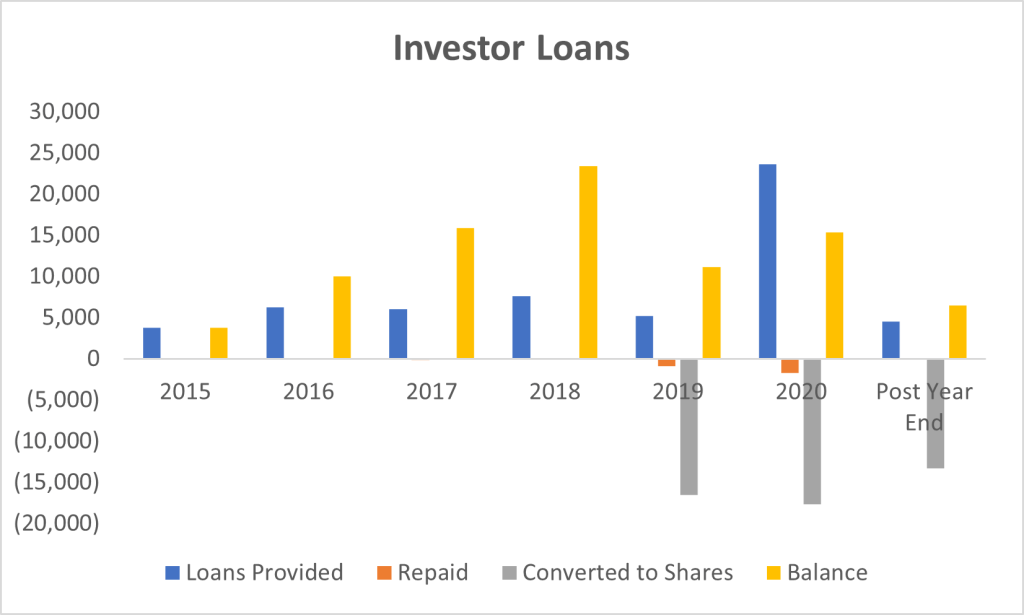

Once again, the current group of investors stepped up, loaning the club a staggering £23.6m in the year, taking the total loans since the 2015 regime change to £52.4m. This is split as follows:

History should view all these individuals very favourably indeed. It is a quite extraordinary amount of money to be invested.

At the year-end (30 June 2020), £15.3m of these loans were ‘outstanding’ meaning £37.1m had been converted to shares over the previous two years. £13.3m of the year-end balance was converted to shares between the year-end and the publication of the accounts (17th November 2020).

In addition, a further £4.5m was loaned post year-end taking total loans provided to £56.9m leaving outstanding investor loans of £6.5m.

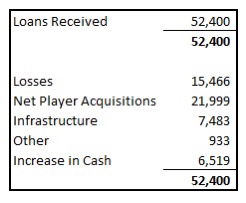

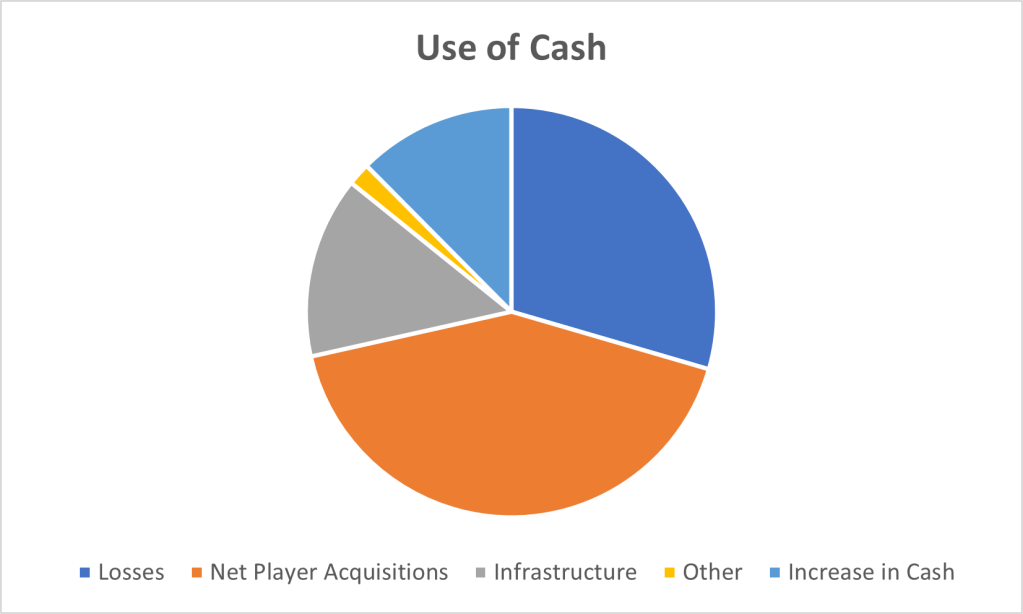

I have laid out how this cash has been spent since FY15. As can be seen below, the investor loans have been used to fund day to day trading losses (£15.5m/30%), net player acquisitions (£22.0m/42%), infrastructure (£7.5m/14%), increase in cash balance (£6.5m/12%) with a small amount used for interest payments amongst other things (£0.9m/2%).

Note – the reason for the difference in figures between infrastructure and player acquisitions here versus previous sections is the timing difference of the amounts in the financial statements (i.e. when the purchase takes place) and the payment – again more on this later.

Legal Disputes

A common feature of Rangers over the last few years has been very public court battles. This financial year was no different with several disputes (old and new) playing out. Firstly, the prolonged battle with Sports Direct. The accounts note that “the company is engaged in ongoing legal proceedings relating to its retail arrangements. Judgment has been granted against the Company in respect of certain breaches of contract but, at this stage, the extent of the Company’s liability other than with regard to legal fees has not been decided by the Court”. It is also noted that “negotiations are ongoing regarding the legal proceedings”.

The club have made a £3.0m provision for these amounts but do stress that there are several uncertainties in arriving at this amount and therefore it may be higher or lower.

Further, the club is engaged in legal proceedings over a dispute with an unnamed former employee. The case is expected to be heard early next year and the Rangers “confident that the hearing will find in favour of the club”.

Further legal proceedings have been initiated by Rangers against Elite for a sum of £2.3m which the club believes it is owed in relation to previous retail operations. No date is noted for this.

Payables

One area to highlight in the accounts is some large payables due. As previously noted, the significant investment in the playing squad is reflected through the payables due to these players previous clubs. Paying transfer fees over instalments is very common with the year end balance of £15.5m due to clubs. Of this, £11.5m is due this financial year. A further £15.4m was spent on players post year-end leaving a significant amount payable.

In addition, Rangers appear to have taken advantage of the Government allowing businesses to defer their VAT payments until the summer of 2021 to allow business to manage their cashflow during the pandemic. Amounts owed to HMRC rose from £2.9m to £9.7m suggesting £6.8m of deferred payments.

Moving forward

Looking forward, the accounts for this financial year will likely show an increased loss in this year on the basis that no players are sold in January. The board estimate a revenue shortfall of around £10m, mainly due to European games being played behind closed doors and with expenditure likely to have increased (i.e., wages) and higher player amortisation charges I would envisage an operating loss north of £20m.

The board have identified that a further £8.8m of funding is required this season with a further £14.4m required the season after. Douglas Park and John Bennett have provided a non-binding guarantee to fund this loss. My own view is that they, and the rest of the investor group, are unlikely to fund the full £23.2m. Instead, this will be met by player sales and/or Champions League football. It is my view that this contains a sizeable amount of risk. There is no doubt that the investment in the playing squad has led to an increased asset base with players that have significant value, but the transfer market contains its own risk – particularly whilst Covid-19 continues to impact on club finances. I was hugely surprised that Morelos was not sold in the summer and there is no way that players will not be sold this summer, if not January. Had we failed to progress in the Europa League this year then phone calls to Lille and Leeds would have been made very quickly.

Our model will replicate Celtic moving forward. On a normal basis, we will run at an operating loss of £10-15m which will be filled by player sales, Champions League football or both. Currently, investors are funding that gap, but we are, in my opinion, close to the end of that being the case.

Of course, Champions League football is the big game changer here and therefore winning the league is imperative to give us the best possible chance to qualify. Given Celtic’s very poor European performances this season so far, it is looking less likely that next seasons Champions will gain automatic entry to the Champions League. However, if that does transpire, next seasons league campaign will likely be the most important in recent times as the winner will have a huge advantage over the other for many years to come.

Ross McAdam

@rossco_bear